Privacy, decentralization, and pseudonymity are central to the crypto ethos and a core tenet of how we guide our investment framework. If DeFi is to fulfill this ethos, there is a massive hole to fill. On-chain TVL is hovering around $60B, which would make DeFi a Top 50 bank in the United States. The growth of lending in DeFi has been rapidly achieved without the development of on-chain credit risk infrastructure.

Over-collateralization was the quick solution for a lack of credit risk infrastructure. Quick fixes are almost always a poor long-term solution, and over-collateralization has led to a number of problems. First, it leads to dramatic capital inefficiencies. Second, it limits loan access to larger “whales” who can provide over-collateralization and furthers inequity as “whales” receive greater governance token emissions. Last, all lending protocol participants are given the same loan terms regardless of credit history and behavior.

Traditional finance’s credit risk infrastructure isn’t perfect either. Credit scoring is gated by an oligopoly of institutions in most Western markets and controlled by the government in other large geographies. Individuals have very little control over their scores and are forced to engage with an opaque, inequitable system. The addressable market for consumer credit services is in the tens of billions, however, even in developed markets like the United States it is estimated that 53mm American adults are unable to generate a FICO score. Decentralizing credit scores will allow Web3 users the opportunity to engage in more accessible and equitable risk infrastructure.

Spectral is focused on filling the credit assessment gap in DeFi by building a permissionless and decentralized infrastructure for Web3 with the vision of globally expanding financial inclusion and access.

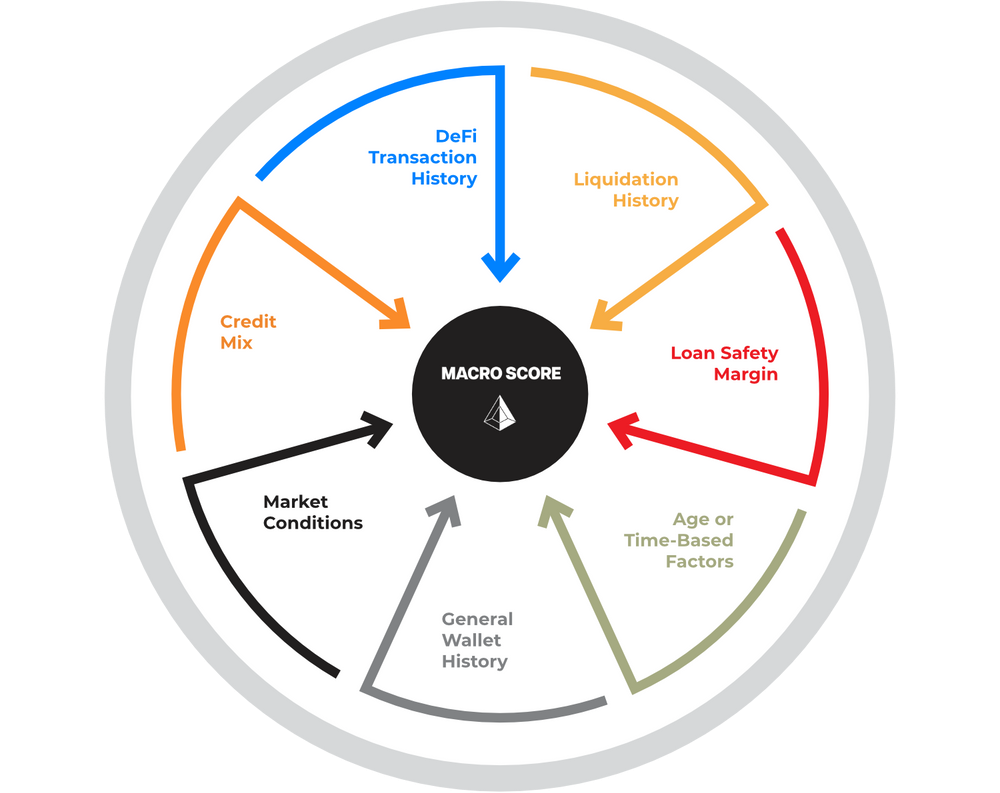

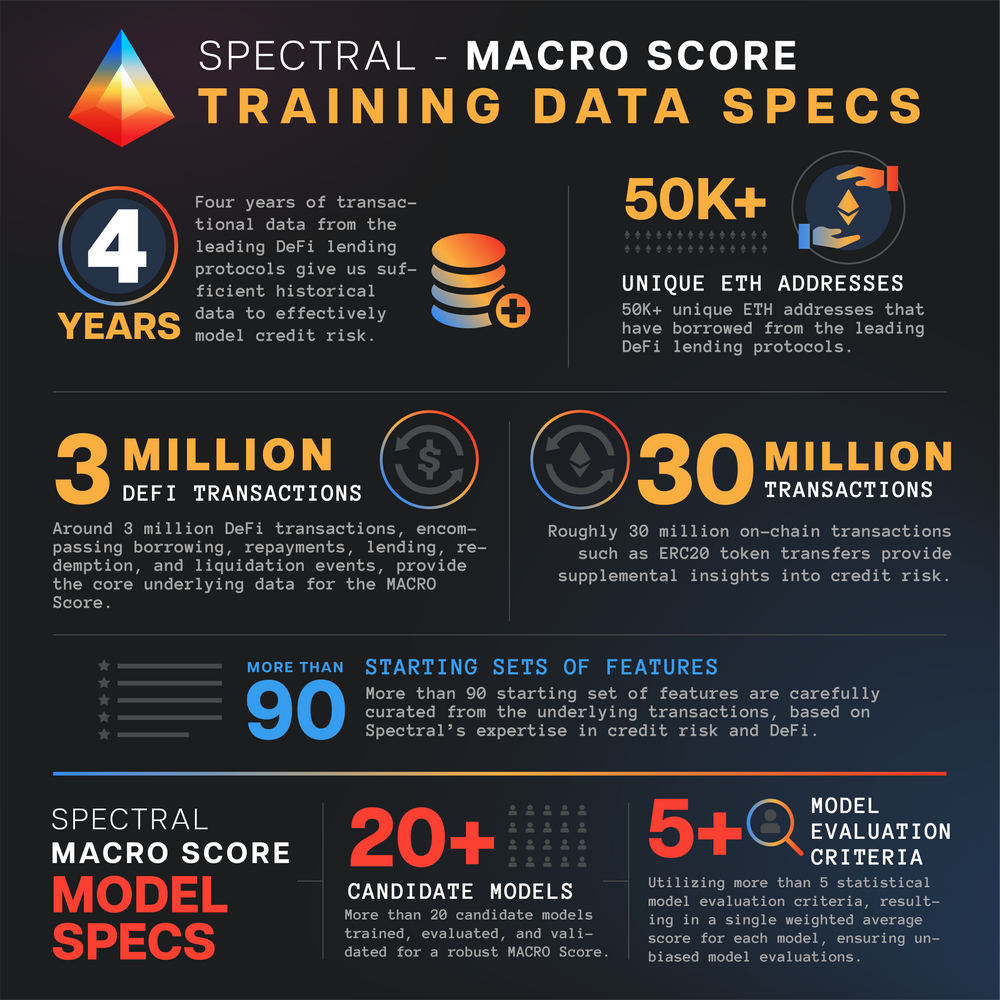

Sequence is important to solving this problem. The team is starting with the launch of their MACRO score, which takes 7 categories of information and over 100 features into account. Spectral’s own machine-learning-based credit risk model processes the complete history of the wallet(s) provided and returns a three-digit representation of on-chain creditworthiness.

The long-term vision, however, is to make credit scoring a publicly accessible network - a decentralized credit risk oracle system that is credibly neutral. Blockchain-based networks brought the world programmable “money”; Spectral’s mission is to build on this achievement and bring the world programmable creditworthiness.

Programmable creditworthiness will enable new use cases on-chain that promote economic inclusion and opportunities. What are some of those use cases? Underwriting for on-chain economies, reducing collateralization requirements, composable and collective scores for DAOs, and more.

The demand for this product speaks for itself. Following the open beta launch a month ago, over 30,000 users have checked their MACRO score - this is just the beginning. In the coming months you can expect integrations of additional DeFi lending protocols, relevant on-chain data sources, and expansion onto other chains (L1s/2s). Decentralization will always be a north star and we are excited to see the addition of community-sourced models to Spectral’s “Scoracle Network.”

There is a massive need for credit risk infrastructure that preserves privacy, decentralization, and pseudonymity. After spending time with Sishir and the Spectral team, it was clear to us that they were aligned on preserving these tenets and would seize the opportunity to build a more equitable system in Web3. This is a hard problem that requires deep engineering and statistical expertise. Beyond that, it was clear to us that the whole team was DeFi power users who possessed first-rate technical skills. We are thrilled to back the Spectral team as they enable Web3 user to take back the control of their financial reputation.

%201.svg)