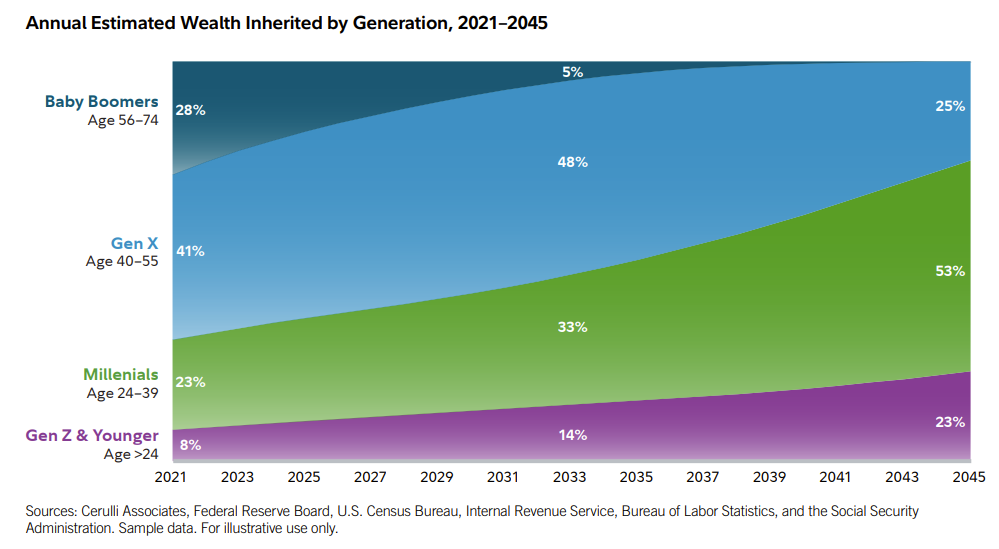

Over the next 20 years, the US will see the largest wealth transfer in history, as Baby Boomers transfer trillions to their heirs. This historic movement of assets represents a unique opportunity for disruptors in wealth management to gain share—something that is usually very hard to do, thanks to extremely sticky client relationships.

As we see it, registered investment advisors (RIAs) have a higher gross retention rate than best-in-class software companies: Once an asset management firm has won a client, the client typically remains on the platform for decades. While this client retention is beneficial for incumbents, this dynamic makes it challenging for startups to quickly gain traction in the space. Until now.

A recent study found that 88% of heirs don’t consider their parents' financial advisors after receiving an inheritance. And given the high retention rate at wealth management firms, this turnover may provide a unique opportunity for new platforms to capture meaningful AUMs.

What will it take for innovations in wealth tech to stick?

Historically, the overarching trend in wealth tech has been creating new solutions that expand access to financial products for the mass affluent. For these solutions to gain substantial adoption—as in fintech in general—we believe they need a great product coupled with an innovative distribution model.

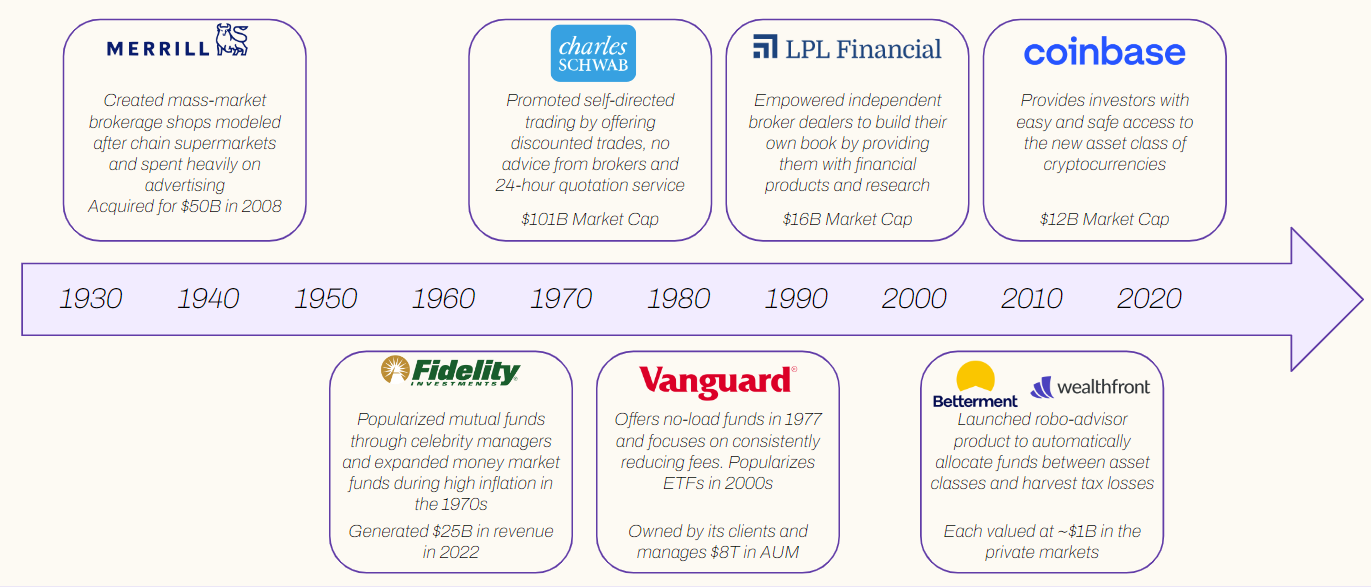

Merrill Lynch and Fidelity are two examples of this winning combination. Fidelity didn’t invent the mutual fund and Merrill wasn’t the first mass market brokerage firm, but each combined new products with innovative distribution models—the promotion of the star fund manager model at Fidelity and the aggressive, yet novel, advertising at Merrill.

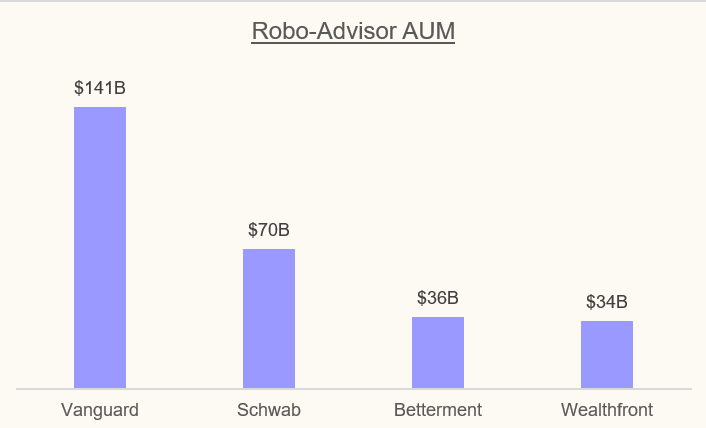

Compare this to what happened to robo-advisors: Betterment created the concept of a robo-advisor and has been able to build a good business, but was unable to gain a distribution advantage. Because Vanguard and Schwab have strong connections with consumers, they were able to copy the innovation and take share.

More recently, Coinbase has been successful here by solving many of the early pain points associated with investing in crypto as well as investing heavily in educating the public on the asset class.

Below is a timeline that highlights a few of the key innovations that have created meaningful value in the industry and helps to understand where the broader wealth tech is heading.

For a more detailed history, we highly recommend Joe Nocera’s A Piece of the Action.

While the fundamentals of great product and innovative distribution hold true throughout the decades, the next generation of clients have very different expectations than those of the past. They’re not looking for an advisor who takes them golfing once a quarter and recommends which mutual fund to invest in.

Understanding what these investors want as well as the best way to reach them is critical to building the wealth tech products of the future.

Opportunities for innovation in wealth tech

Younger consumers have different expectations of what wealth solutions should be than has been traditionally offered. In order to reach them, products will need to offer a completely redesigned experience. A great UX, access to different asset classes, full banking features, and direct indexing will all be table stakes. Next-generation wealth tech should reflect these elements and augment them with AI-based advice.

Digital-first

Unsurprisingly, young investors are far more comfortable with digital experiences and approximately half are open to using a robo-advisor. However, despite the prevailing belief that young consumers prefer to interact only with automated solutions, more Gen Z and Millennial investors than those from older generations indicated they would want an advisor they speak with fairly frequently. This suggests that in order to retain clients—especially as they increase their wealth—a human element is necessary as a complement to the digital experience.

Multi-functional

The lines between trading, asset management, and banking are blurring. As a result, younger investors want a combined solution that encompasses all three. While the meme stock-fueled trading has died down, young investors still want to trade on their own account and FOMO remains a driving force.

Access to diverse asset classes

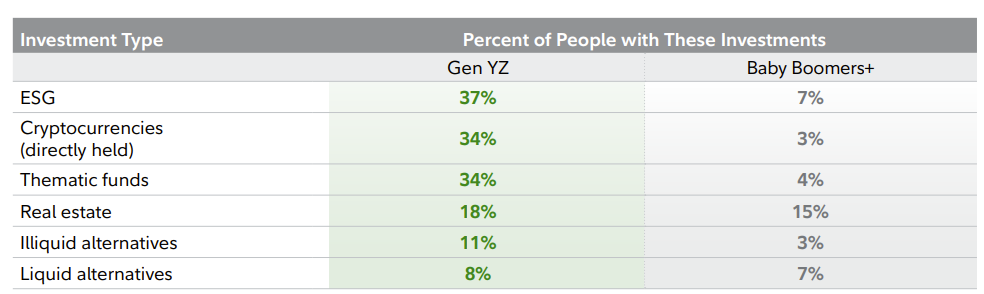

Next-gen investors also want a more diversified set of assets in their portfolio. The difference in portfolios across generations is driven by a focus on representing investors’ beliefs in their investments as well as the emergence of new tools providing access to asset classes like crypto and private investments.

Comprehensive, personalized, and powered by AI

The rise of ETFs and robo-advisors has fully commoditized portfolio construction, so simply providing portfolio advice is not enough. Younger consumers are looking for a more comprehensive solution—one that tackles financial planning holistically to help them achieve their life goals.

In order to capture an investor’s full share of wallet and provide truly comprehensive advice, wealth tech applications need to provide investors with powerful research tools to make their own investing decisions. This is where we believe thoughtful applications of AI can create enormous value. There is an enormous amount of data available on public assets across company filings, equity research, and social platforms, but most casual investors don’t want to sift through filings to learn about a company. A product could provide both a quantitative research portal combined with qualitative analysis leveraging AI tools. Further, these tools could synthesize structured and unstructured data to provide financial coaching. As the model ingests more data and can build a more accurate profile, it will be able to provide far more personalized advice than can be found online.

For example, an investor might ask “How much should I invest in crypto?” A range of “experts” online recommend investing between 1% and 5% of your net worth. But this is a broad range and doesn’t reflect any information about the investor’s circumstances. By understanding an investor's goals, relationship with money, and projected income, a wealth tech product can provide more relevant advice delivered with the context of why it provided the specific recommendation.

But building an AI-based financial advisory platform is not as straightforward as simply embedding GPT-4 into an existing solution. The challenge of hallucination is acute across all financial services—which is why ChatGPT does not provide direct financial advice. Additionally, to become a fiduciary and monetize on an AUM basis, an organization has to provide advice that is in the client’s best interest. This advice must be defensible and consistent (e.g., if two clients in the same situation ask the same question, the advice should be the same). Given these models operate in a “black box”, platforms should use these tools to ingest unstructured data as one input into the underlying model but not power their entire solution.

What’s the wedge?

A “wedge” product is one that initially onboards a customer and then builds sufficient trust for them to expand their usage. The activation energy required to move all assets onto a new wealth platform is extremely high and thus the platform needs to demonstrate its initial value with a single product. Below are two examples of wedge products that we think could capture a greater share of a consumer’s financial life.

Tax strategy

Most mass-affluent consumers are focused on taxes once a year when they send their forms to an accountant or file through an online platform. Filing taxes and finding refunds has become commoditized, but there are additional small steps these consumers can take throughout the year to lower their bill. This is particularly true for consumers who receive equity as part of their compensation, have an additional source of income, or are going to receive an inheritance. An AI model would be well-positioned to provide this service.

This AI product would be an attractive wedge because tax advice has clear and immediate ROI and requires deep integration into a consumer’s entire financial stack.

Inheritance support

The technical process of receiving an inheritance can be extremely difficult and stressful, particularly at such a difficult period of time. With multiple accounts and recipients, just transferring liquid financial assets can be challenging and the difficulty increases by an order of magnitude for illiquid assets such as real estate.

By facilitating the inheritance, an inheritance product would be a well-positioned wedge to bring these assets onto a larger platform. Plus, simplifying this pain point is a great way to build a trusted relationship with a customer.

What distribution strategies might win?

For all products in financial services, trust is the most important asset, and nowhere is this more true than in wealth tech. Product innovation without a distribution unlock isn’t sufficient.

For founders building in the wealth tech space, there are two main distribution approaches to consider: direct to consumer (DTC) and distributed through advisors. Each comes with their own advantages and disadvantages but both offer a path to scale.

Direct to consumer

The benefits of going DTC is that the platform captures all of the economics and can be scaled if the go-to-market (GTM) efficiency metrics are attractive. Both traditional and next-gen wealth tech products have extremely high retention rates though often have long payback periods due to the cost associated with converting consumers to move their wealth.

As an aside: If you are a founder building in this space, General Catalyst’s Customer Value Strategy can be a value unlock in this regard. Depending on the circumstances, it might not make sense to finance the acquisition of these predictable and stable customers with expensive equity.

The critical question with the D2C model as applied to wealth tech is: “will higher net worth clients be willing to use an automated solution?” The ability to retain a user when they inherit wealth and move up the wealth bracket or start earning meaningful income is paramount.

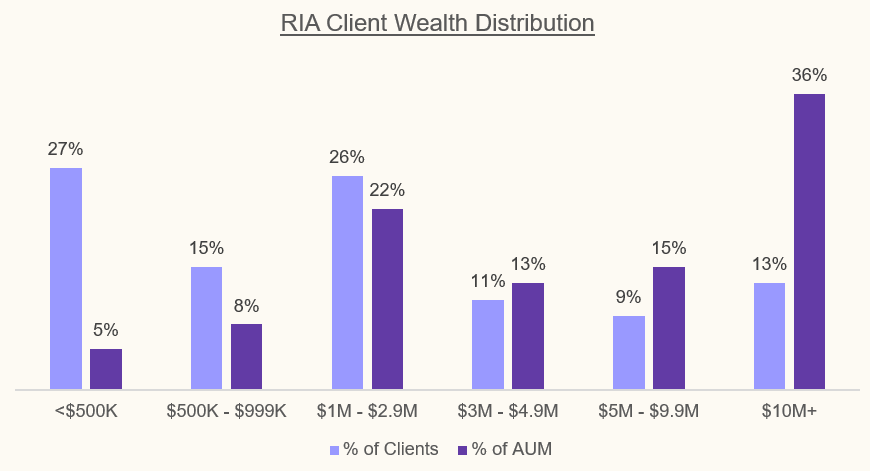

Not surprisingly, at traditional RIAs the majority of AUM is driven by a minority of clients. Fully-automated wealth platforms will have the advantage of being able to serve clients in lower wealth brackets profitably, but the challenge will be gaining enough scale. To be successful in going DTC in this category, a disruptive player will have to invest heavily in their brand in addition to standard targeted Instagram and Google ads. Chime and SoFi are examples of new players who have done this well via stadium sponsorships and Coinbase who has strongly invested in national TV ads including a memorable 2022 Super Bowl ad.

One of the advantages of serving a younger client base is that they refer three times more clients than older generations. Wealth tech is primarily a single-player experience, but younger clients’ willingness to refer their advisors to their peers indicates a high-quality product may be able to unlock organic growth via word of mouth.

We think building in DTC wealth tech with a target audience of upwardly mobile young investors can be extremely profitable but will require a team that can not only build an amazing product, but also a brand that resonates with this consumer.

Advisor-led distribution

The other approach to distribution is via advisors. There are a few interesting trends in the advisor market that could make this a compelling option.

First, independent advisors are gaining share and are easier to sell solutions into than the largest banks and wirehouses, which are known for long sales cycles as well as hesitancy to work with more innovative solutions. (Source: McKinsey)

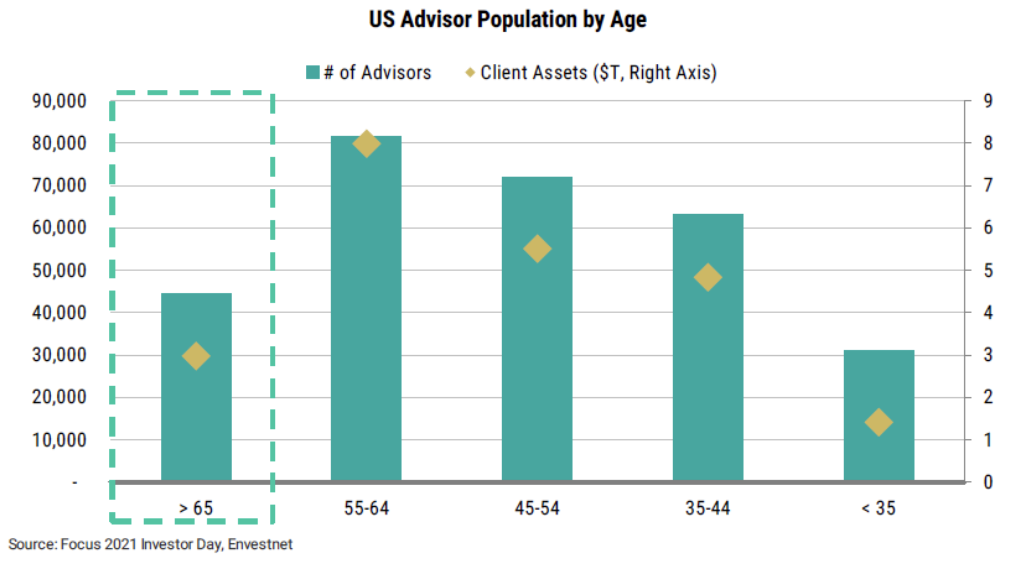

Second, and in addition to the change in client demographics, many advisors are also likely to retire in the next decade. There are 45,000 advisors in the US over the age of 65 servicing $3T in AUM. This presents a large opportunity to build solutions for younger advisors as they gain market share and increasingly build out their book of business.

Third, distributing through advisors augments the AI solution with the reassurance of a trusted relationship. Even though the human advisor probably wouldn’t provide any advice that the AI-powered solution wouldn’t offer, consumers may want to confirm the AI’s work with someone they trust.

Selling solutions into RIAs has its challenges as they are often using a myriad of products and replacing the entire stack is a challenging rip-and-replace sales motion.

A few startups have been successful in selling into RIAs—such as Altruist—but others have taken a different approach: recruiting advisors to build an RIA in-house and building solutions for their advisors. RIA roll-ups can be quite profitable and these startups can achieve superior returns by building advanced solutions to empower their advisors.

Selling into advisors and building new advisor platforms offer compelling approaches for an advisor-led distribution strategy. While most of the new solutions have been targeted at advisors, builders must focus on the end customer as well. To be successful with an advisor led-distribution strategy, products should be built for both the advisor and the client.

We want to hear from you

We are at the perfect time to build new wealth tech solutions from the ground up serving more tech-savvy consumers who have different expectations than previous generations. At the same time, advancements in AI will allow companies to build entirely novel products, increasing the reach and at the same time personalization of the advice. There are a few distribution approaches that could be successful but founders need to be extremely thoughtful about how to gain massive scale in a space that requires immense consumer trust.

If you are a highly technical team that is building in this space with the goal of building a generational company, please reach out to us at General Catalyst!

%201.svg)