Less than a year ago, we wrote about why AI-enabled roll-ups (a model for services transformation that pairs applied AI with strategic acquisitions of service businesses), could reshape the services economy. The thesis was global. The proof points were early. We argued that the biggest near-term impact of AI wasn't going to be in software but in services, and that the right response wasn't to sell software into those industries, but to drive transformation from within by becoming a service provider.

Today, that thesis holds. And our key insight since publishing has been this: the conditions that make AI roll-ups work are more concentrated in Europe than anywhere else.

This is the European chapter of that story. We trace why the structural conditions here are uniquely suited to AI transformation in services through a roll-up strategy, what we've learned with Dwelly (a UK-based lettings & property management AI-first platform), and what it means for founders across the continent looking at fragmented, analog industries asking the same question we did three years ago.

A Global Strategy with a European Edge

GC's Creation strategy has been helping build thesis-driven companies from the ground up for over 25 years, some becoming category-defining companies like Livongo (acquired by Teladoc in an $18.5 billion merger), Kayak, and Commure. Our creation strategy has evolved to support two modes: hatching new companies with talented founders in nascent industries, such as Hippocratic AI, and what we now call Transformations - backing founders to acquire, rebuild, and operate legacy service businesses using AI as the primary lever.

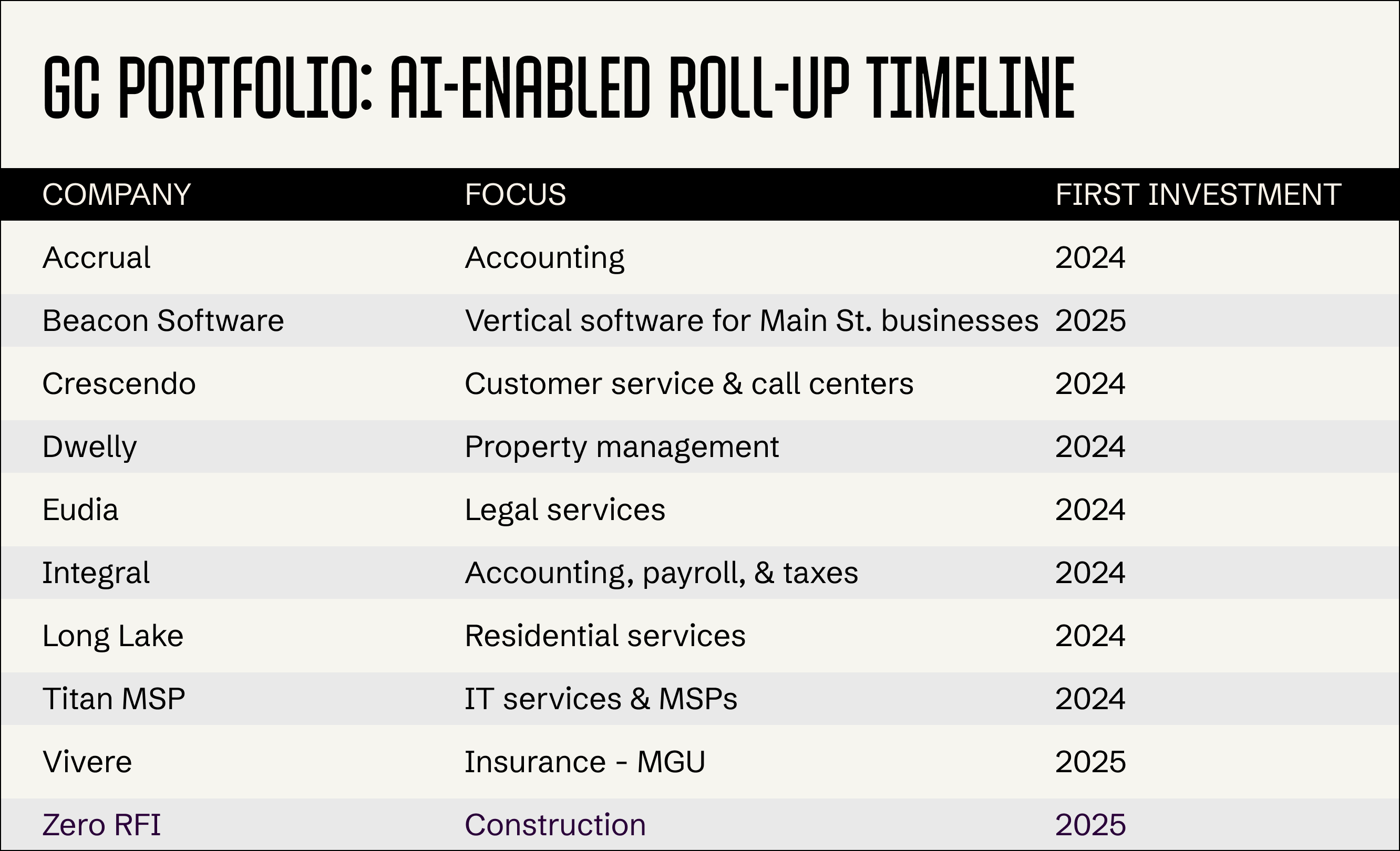

We've created and invested in many companies pursuing AI-enabled roll-ups, including: Accrual, Beacon Software, Crescendo, Dwelly, Eudia, Integral, Long Lake, and Titan MSP. We expanded the Creation Fund from $800 million in Fund XI to $1.5 billion in Fund XII because we believe the opportunity in AI-era company-building is larger than ever. That's the global context. But the European opportunity has its own distinct shape.

What This Is Not

The most common response when we describe AI-enabled acquisitions is still: "That sounds like PE." It is not. This is an AI transformation and product reinvention strategy, not a PE roll-up. We seek to partner with exceptional technical and product minds to rebuild how services are delivered and to create new products that can achieve better outcomes for customers. Acquisitions are simply the fastest path to customers.

PE roll-ups typically use leverage and cost extraction to create equity value: acquire, consolidate overhead, reduce headcount, service debt. AI-enabled roll-ups invert that logic. We generally invest upwards of $100 million in these businesses and deliberately add costs for technology build, platform development, and integration work, because we're rebuilding the value chain, not optimizing the existing one.

We partner for the long term, unlike PE’s typical three-to-five-year horizon, because real transformation takes time, and compounding requires patience. At the core is a venture mindset: building and operating companies for power-law outcomes that reshape entire sectors.

Why Europe, Why Now

In 2023, we asked a simple question: where will AI have its biggest near-term impact? The answer wasn’t software but services, particularly in Europe’s $4T+ information, professional, and administrative sectors, which run largely on text- and voice-based workflows. In areas like accounting, legal, and real estate, AI expands what these businesses can deliver. By removing repetitive work, it frees professionals to apply more judgment, effectively increasing the value delivered and size of the market itself.

Today, we’re entering a new phase of applied AI where the center of gravity is shifting from tools that assist humans to systems that directly deliver outcomes. Every applied AI company aspires to make this transition, but AI services companies start there by design. When you sell a service, you are not selling software; you are selling the outcome. That positioning matters because it embeds the company directly in the execution of the work, where the most valuable learning happens.

By operating in the flow of real tasks, AI services companies create a continuous feedback loop between customer intent, execution, and outcome. Each job completed, each edge case encountered, and each customer reaction becomes a training signal, refining capabilities and its judgment. The shift from copilot to autopilot occurs through learning-by-doing. The product improves because the service is being delivered, and the service improves because the product is learning. Over time, this creates a self-reinforcing system in which performance compounds with use. This advantage is built on accumulated, domain-specific experience.

AI services companies are uniquely positioned in this paradigm shift. By starting with outcome delivery, they tap directly into existing budgets and customer demand for results. They place themselves at the point where intelligence is created, in the act of doing the work.

European markets offer structural advantages to deploy AI transformation through a roll-up. SMEs form the backbone of Europe’s economy:

- In UK real estate, where Dwelly is leading an AI-enabled rollup, 60% of the market is made up of 3,000+ agencies, each generating under £3 million in revenue.

- In Germany, 90% of property management firms earn less than €5 million, and in SME accounting, where Integral is driving an AI rollup, 40% of firms make under €3 million with no clear national leader. Large markets, deep fragmentation, family ownership, generational succession with no obvious path forward.

For AI-enabled roll-ups, small companies are structurally primed for transformation that can fundamentally change their unit economics. These businesses are often family-owned and are now facing generational handover. AI rollups can offer both a succession solution and a cultural upgrade, empowering employees to embrace technology, modernize operations, and become co-owners. Founders in Europe have a unique chance to define local market leadership, drive network effects, and consolidate fragmented verticals efficiently.

There's also a broader imperative. As AI reshapes global service delivery, European companies face a real choice: offshore to lower-cost markets, or transform with AI to compete on quality and capability. AI-enabled roll-ups offer a third path - keeping value creation, jobs, and productivity in Europe while raising the standard across entire industries. It's central to why building this here matters.

Dwelly: The Proof Point

When Ilia, Dan, and Dmitry came to us with Dwelly, the pitch was to roll up UK letting agencies and rebuild them with AI. What made it worth backing was the team - Uber and Gett veterans who understood high-growth operational complexity - and the industry insight specific to the UK market: rental contracts last three to five years, making organic customer acquisition nearly impossible. The window when a landlord is between agents is too narrow. Acquisition is the only viable route to scale. Buy the customer base, then transform it.

In under two years, Dwelly has signed more than 15 agencies, crossed 10,000 properties under management, and reached a scale placing it among the UK's top 15 largest letting agencies - a pace the industry rarely sees.

The operational results are evidence of our thesis at work. According to Dwelly, time to find a tenant drops from the industry standard of three weeks to under two days. Maintenance resolution times are down by a third, targeting over 70% reduction. Manager productivity has doubled. More than 80% of Dwelly's customers now go through the entire rental process via the chatbot without speaking to a human agent.

That last number is worth pausing on. In the UK, estate agents operate under administrative burdens that make good service structurally difficult, shaping their reputation. Dwelly removes the ceiling that was preventing them from doing their jobs well.

Lessons for Europe

We’ll close by sharing lessons for European founders thinking about building here:

- This is an AI transformation and product reinvention strategy, not a PE roll-up. We partner with exceptional technical and product minds to rebuild how services are delivered and to create new products that achieve better outcomes for customers. Acquisitions are simply the fastest path to customers. The industry defaulted to AI as a cost tool. The shift we are driving is toward AI as a growth engine. This is only possible when a team approaches the problem with a technology- and product-first mindset, pairing execution capability with a commitment to improving customer value.

- The team is the key ingredient that determines success: AI rollups are complex, involving three builds: a proprietary AI platform, an acquisition engine, and a redesigned delivery model. You need a team that’s done it before - a technologist-operator pair: one leading AI and product, the other running integration and M&A. Dwelly’s founders had built together before and worked at Uber. Integral’s founders previously co-founded Penta, Germany’s leading SME neobank, and now use that experience to transform SME accounting. Deep domain expertise is essential, either within the founding team or through the first acquisition.

- Automation metrics lead. Financial results follow. Capital has to support the gap between them: The KPIs that matter first are operational: AI work-hours generated, tasks processed without human intervention, and agent time freed. Dwelly's margin expansion came after the platform was deployed, not before. Crescendo's gross margins came after automating customer interactions. Set automation targets first. Your capital structure has to support a period where costs rise before returns do.

- Market fragmentation in Europe is the perfect market condition for AI transformation through a roll-up strategy: Most major European service sectors share the same profile: large markets, extreme fragmentation, family ownership, succession pressure, and no technology layer. That's what makes an acquisition-led transformation strategy viable. Founders in Europe have a unique opportunity to define local market leadership, drive network effects, and efficiently consolidate fragmented verticals. Start by building a local champion with the foundations to scale pan-European - AI now enables service and care across the EU by abstracting away language and cultural differences.

The Window Is Open

Across eight active AI services transformations, GC's portfolio is already showing what the next generation of European services companies looks like. The question is who captures the next category leaders across Europe’s fragmented, analog industries before the window narrows. The founders who move now, with the right team and capital, will shape these industries for the next generation.

What we have seen work in property and customer service, we expect to see replicated across professional services, insurance, accounting, and property management across Europe. Those who move early will set the terms for those who follow.

%201.svg)